Authors: Bruno Kezeya; Cecilia Antoni; Marcus Mergenthaler

Production and uses

Grain legumes have several agronomic, environmental and dietary benefits. Surprisingly, they play only a minor role in today’s farming systems as well in human nutrition in the EU. In fact, dry grain legumes represent only 2.1 % of arable land in the EU – but with an increasing trend. Legumes with their high protein content could play a key role to reduce the EU dependency on protein imports. To achieve this goal, the area under legumes should increase. The reasons why legumes do not measure up to their potential yet, are manifold. One key factor is that there is a lack of competitive and sustainable value chains which are able to meet respective demand potentials. Another one is the lost knowledge about the preparation and tradition of pulses as human food.

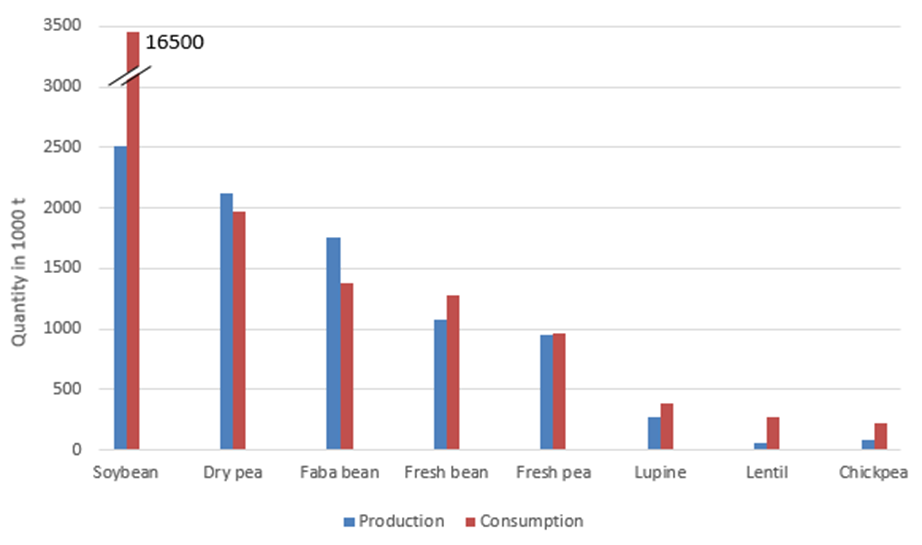

Nowadays, the soybean is the main produced grain legume in the EU, followed by dry pea and faba beans (see fig. 1). These three crops and lupins have multifunctional uses, mainly for feed, followed by an increasing trend for food, and also as Biofuel (as it is the case for soybeans in Italy). Soybeans are mostly grown in the southern countries of Europe namely Italy, France, Romania, Croatia, Austria and Hungary. The other grain legumes are mainly grown in the north of the continent in countries like the UK, Germany, Poland and Lithuania. Beside this group of grain legumes, there is also the group of dry grain legumes with exclusive use for food. This includes chickpea, lentil and common bean. The demand of these grain legumes is covered by imports, mainly from America (USA, Canada, Mexico and Argentina). Worldwide, grain legumes are largely cultivated in conventional farming. Less than 1 % of the global dry legumes´ areas are under organic management.

Fig. 1: Yearly average production and consumption of grain legumes in the EU from 2014 to 2018.

Trade and consumption:

Soybeans: Germany, Spain, Netherlands and Italy are the main consumers of soybeans in the EU. The production in these countries remains lower than consumption. Soy´s imports are mainly from the USA and Brazil and soy meals are mainly imported from Argentina and Brazil. Still most of the soya is used as animal feed.

Dry peas: France is the first producer of dry peas in the EU, followed by Germany, Lithuania, Romania and Spain. Spain, France, Germany and Italy are the main consumers. The EU is a net importer of peas, namely from Russia and Ukraine.

Faba beans: UK is the first producer of faba beans in Europe, followed by France, Germany, Lithuania and Italy. These countries belong to the main consumers, too. The EU is a net exporter of faba beans, principally to Egypt for food and Norway for fish feed.

Chickpeas: Spain is the first producer and consumer of chickpeas in the EU. In term of production, France, Italy, Greece and Bulgaria follow Spain. In term of the consumption, the UK, Italy and France follow Spain. The imports are from North and South America.

Lentils: Spain and France are the main European producers and consumers of lentils in the EU. In terms of consumption, Italy, Germany, UK and Greece follow. Canada is the principal supplier of lentils to the EU. The signs of origin and quality of lentils characterized its production in the EU.

Economic of grain legume:

The fluctuating yield of pulses is a factor that affects the profitability of legumes. Further efforts should be made in breeding for this purpose. The economic benefits of legumes derive from their lower production costs compared to those for cereals. Considering the entire crop rotation with legumes, the quantification of economic benefits of legumes is more attractive than crops rotation without legumes. Unfortunately, in many farm level calculations, the economic viability of legumes does usually not relate to the entire crop rotation. Therefore the economic benefits are often underestimated. The isolated low profitability of grain legumes is also due to low market prices. Low market prices are caused, among other factors, by information asymmetries and market power between actors. The use of price indicators might help to increase market transparency. The import of GMO-soybeans and soy meal as alternative sources of protein for feed is another reason why the price of certain legumes like peas, faba beans and lupines is less attractive.

Due to the increasing trend of vegetarians and vegans, there are more and more processors that extract protein from grain legumes for the production of meat- and milk-free food. The continuous demand from this market segment might lead to an increasing of price level of grain legumes. The food market segment requests a higher quality than in the use for feed. The market price of faba bean, dry pea and lupin in food as compared to feed is more profitable for farmers. As feed processors push prices downwards, some farmers use legumes in their own compound feed mixing. As they avoid market transactions, this is called “intra‐farm‐use”. Alternatively, farmers directly sell legumes for feed to their neighbouring livestock farmers, leading to “inter‐farm‐use” of legumes.

Sources:

- Legumes in the EU: https://www.legvalue.eu/media/1511/d31-report-on-legume-markets-in-the-eu.pdf

- Soybeans markets: https://www.legvalue.eu/media/1915/legvalue-fiche-soja-juillet-2021-eng.pdf

- Dry peas market: https://www.legvalue.eu/media/1914/legvalue-fiche-pois-juillet-2021-eng.pdf

- Faba beans market: https://www.legvalue.eu/media/1916/legvalue-fiche-feverole-juillet-2021-eng.pdf

- Chick peas markets: https://www.legvalue.eu/media/1918/legvalue-fiche-pois-chiche-juillet-2021-eng.pdf

- Lentils markets: https://www.legvalue.eu/media/1917/legvalue-fiche-lentille-juillet-2021-eng.pdf

- Price indicators: https://buel.bmel.de/index.php/buel/article/view/226/pdf;

- FN_06_Verwertungsdifferenzierte_Preisberichterstattung_Futtererbsen_und_Ackerbohnen._Aktualisierung_der_Soester_Preisindikatoren_fuer_Koernerleguminosen.pdf (fh-swf.de)